Borrowing money is sometimes necessary to cover unexpected expenses, consolidate debt, or finance important purchases. Two of the most common borrowing options available to consumers are personal loans and credit cards. Both financial tools provide access to funds, but they function differently and are suited for different financial situations.

Understanding the differences between personal loans and credit cards can help individuals choose the most cost-effective option based on their financial needs, repayment ability, and spending goals.

What Is a Personal Loan

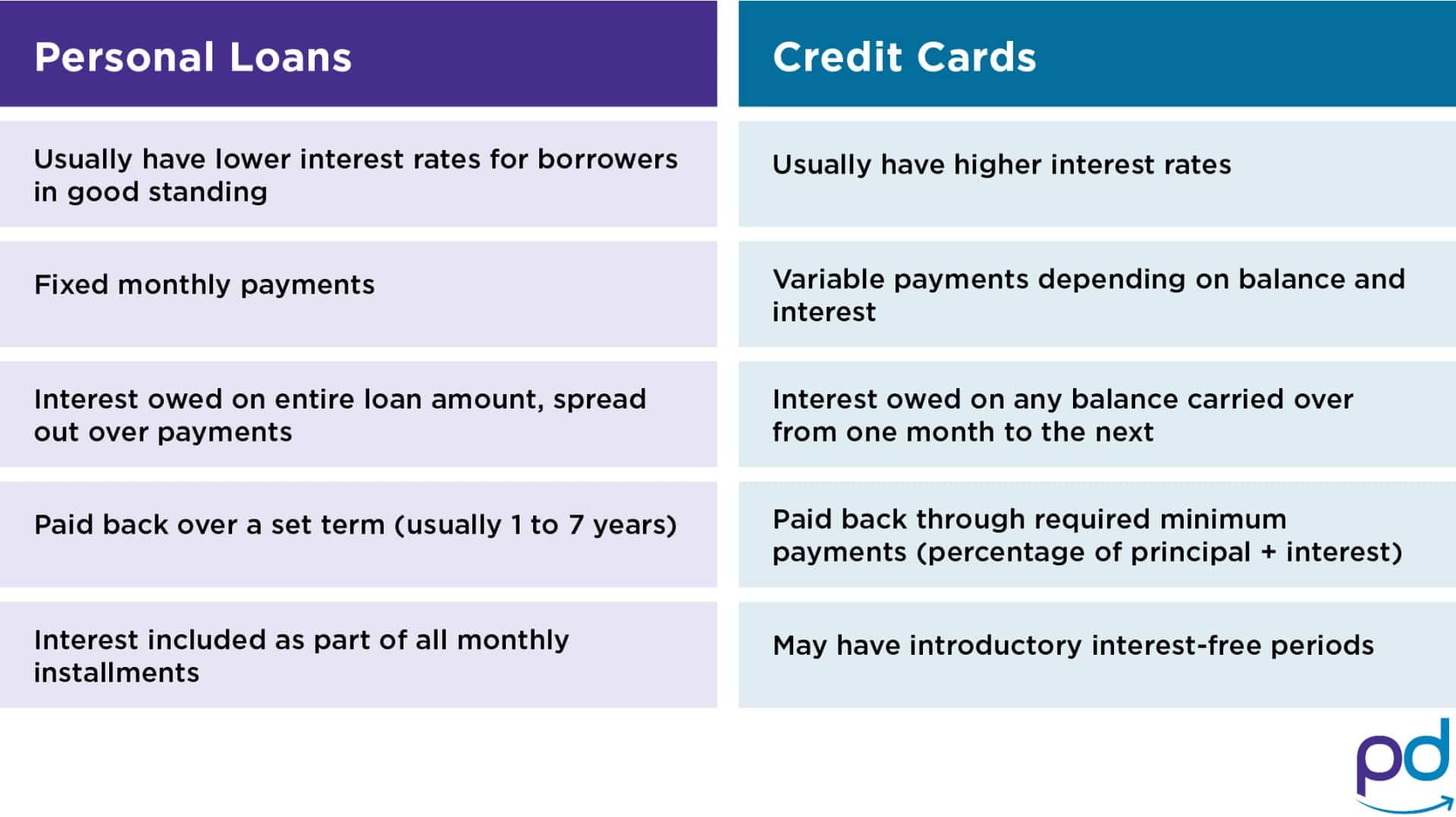

A personal loan is a type of installment loan where a lender provides a fixed amount of money that must be repaid over a predetermined period of time. Borrowers typically repay personal loans in monthly installments that include both the principal amount and interest.

Personal loans usually come with fixed interest rates and structured repayment schedules, which makes budgeting easier. Loan terms typically range from one to five years depending on the lender and the borrower’s credit profile.

Personal loans can be used for many purposes including debt consolidation, home improvements, medical expenses, or major purchases.

What Is a Credit Card

A credit card provides a revolving line of credit that allows users to borrow money repeatedly up to a specific limit. Unlike personal loans, credit cards do not provide a fixed lump sum of money.

Credit card users can make purchases, repay a portion of the balance, and continue borrowing as long as they remain within their credit limit. Most credit cards require a minimum monthly payment, but users can choose to pay off the full balance to avoid interest charges.

Credit cards often come with additional features such as cashback rewards, travel points, fraud protection, and purchase protection.

Key Differences Between Personal Loans and Credit Cards

One of the main differences between personal loans and credit cards is the borrowing structure. Personal loans provide a one-time lump sum payment that must be repaid over a fixed term. Credit cards offer continuous borrowing access as long as the credit limit is not exceeded.

Interest rates also differ significantly. Personal loans typically offer lower interest rates compared to credit cards, especially for borrowers with good credit scores. Credit cards generally have higher interest rates, particularly when balances are carried over month to month.

Repayment flexibility is another difference. Personal loans require fixed monthly payments, while credit cards allow borrowers to make minimum payments or pay off the full balance.

When a Personal Loan Is the Better Option

Personal loans are often the better option for large expenses that require a structured repayment plan. Because personal loans usually offer lower interest rates than credit cards, they can be more cost-effective for significant borrowing needs.

Debt consolidation is another common reason people choose personal loans. Borrowers can combine multiple high-interest debts into one single loan with a lower interest rate and fixed monthly payments.

Personal loans also provide predictable repayment schedules, which can help individuals manage their finances more effectively.

When a Credit Card Is the Better Option

Credit cards are better suited for smaller purchases and short-term borrowing needs. Many credit cards offer a grace period where users can avoid paying interest if the balance is paid in full each month.

Credit cards are also useful for everyday spending because they provide convenience and reward programs. Cashback and travel reward credit cards can offer valuable incentives for regular purchases.

Another advantage of credit cards is quick access to funds. Users can make purchases immediately without applying for a new loan each time they need money.

Impact on Credit Score

Both personal loans and credit cards can affect your credit score in different ways. Responsible use of either borrowing option can improve your credit profile.

Personal loans can help diversify your credit mix and demonstrate your ability to handle installment debt. Making consistent on-time payments can strengthen your credit history.

Credit cards influence credit utilization ratio, which is the percentage of your available credit that you are currently using. Maintaining low credit utilization and paying balances on time can help improve credit scores.

Interest Rates and Fees

Interest rates play a major role in determining the cost of borrowing. Personal loans generally offer lower interest rates compared to credit cards, especially for borrowers with strong credit profiles.

Credit cards often come with higher annual percentage rates, but some cards offer introductory zero-interest periods for new purchases or balance transfers.

Borrowers should also be aware of additional fees such as late payment fees, balance transfer fees, and annual fees when evaluating credit cards.

Tips for Choosing the Right Borrowing Option

Selecting between a personal loan and a credit card depends on the size of the expense and how long you expect to take to repay the borrowed funds.

For large planned expenses with long repayment periods, personal loans often provide lower interest rates and structured payments.

For smaller purchases or short-term borrowing needs, credit cards may offer greater convenience and flexibility.

It is also important to compare lenders and credit card offers before making a final decision. Reviewing interest rates, fees, repayment terms, and reward programs can help identify the most cost-effective option.

Personal loans and credit cards are both valuable financial tools when used responsibly. Personal loans provide structured repayment plans and lower interest rates for larger expenses, while credit cards offer flexible borrowing and rewards for everyday spending. By understanding the strengths and limitations of each option, borrowers can choose the financial solution that best matches their needs and maintain better long-term financial health.